The fate of struggling social network MySpace could soon be decided, following rumours of a buyout by online advertising company Specific Media.

News Corp, which bought MySpace for $580 million in 2005, announced in February that it intended to sell the company by the end of its fiscal year (30 June). The media conglomerate had hoped to rake back around $100 million (£62m) from the sale, but sources told The Wall Street Journal that MySpace is only expected to fetch around $35 million (£22m) in cash and stock.

MySpace is expected to shed more than half of its 500 members of staff as part of the deal, which could be announced as soon as Wednesday, one of the people familiar with the matter told the Wall Street Journal. This follows an earlier 30 percent staff reduction in April 2010, and a further cut of 47 percent in January 2011.

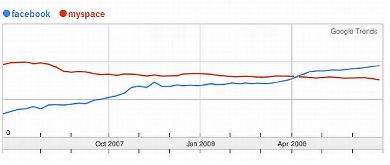

MySpace first appeared in 2003 and, by the time Facebook (then known as thefacebook.com) launched the following year, it already had a million members. By the end of 2004, Facebook had reached the million mark but MySpace had rocketed to five million members. Facebook continued to trail behind MySpace until April 2008, by which point MySpace subscriptions had begun to flatten out.

This prompted a major development programme by News Corp, which started to pile in new features to make music more accessible and to allow customisation of its pages. However, rather than popularise the social network, the extra features started to slow down page access speeds and, gradually, people began to leave MySpace and switch to Facebook.

Since 2008, Facebook has surpassed 500 million members, but MySpace has remained stuck around the 125 million mark. According to comScore, this number is eroding fast and the unique visitor rate has decreased in the past year to around 60,000 last February.

“Social networking is much more than a trend, it is a reality. Consumers have embraced this phenomenon and those companies benefiting from this are raising significant capital either through private placements and via the public markets (IPO). While some valuations may seem excessive at face value, a number of these companies such as Facebook and Zynga are one-of-a-kind and will continue to grow exponentially,” he added.

Earlier this year, professional social network LinkedIn went public, with an initial public offering (IPO) of $175 million (£110m). The company’s share value more than doubled on its first day of trading, but LinkedIn warned in a regulatory filing that its growth rate is likely to slow as the company boosts spending on technology.

Meanwhile, Facebook has racked up $1.5 billion (£929m) in funding to date from Goldman Sachs and Digital Sky Technologies. However, most expect that investment to pay off exponentially, with social advertising booming and Facebook’s “Like” button spreading across the web.

Some experts expect the company to file an IPO by 30 April 2012, when it will have to disclose its finances under SEC rule.

Suspended prison sentence for Craig Wright for “flagrant breach” of court order, after his false…

Cash-strapped south American country agrees to sell or discontinue its national Bitcoin wallet after signing…

Google's change will allow advertisers to track customers' digital “fingerprints”, but UK data protection watchdog…

Welcome to Silicon In Focus Podcast: Tech in 2025! Join Steven Webb, UK Chief Technology…

European Commission publishes preliminary instructions to Apple on how to open up iOS to rivals,…

San Francisco jury finds Nima Momeni guilty of second-degree murder of Cash App founder Bob…

{kind=link}

{kind=link}